by John Egan

Updated July 8, 2024

In a nutshell

Getting started with investing can feel a little overwhelming if you’ve never invested before. This guide can put you on the right path, though, outlining 10 of the best ways for a newbie to invest money ranging from high-yield savings accounts and workplace retirement plans to mutual funds and exchange-traded funds (ETFs).

High-yield savings accounts, money market accounts and

certificates of deposit have recently started offering yields

above 5% annually.

Bonds may provide slightly higher yields

than savings accounts.

Stocks are the most risky investments,

but they can provide higher returns over the long term.

11 ways to invest money for beginners

1. Micro-investing that turns extra money into an investment

The quickest and most painless way to start investing is by putting aside a small amount of money every day. Several apps allow you to link a bank account and roll over a small amount of money on a schedule you set. As you accumulate funds, you can either chose more direct or more hands-off investments, depending on your level of interest. For beginners, this "set it and forget it" strategy is a good way to keep on a steady course and grow your wealth.

2. High-yield savings accounts

A high-yield savings account enables you to earn far more interest than you could with a traditional savings account. As a result, it’s an ideal component of an investment strategy for beginners.

As of April 2024, some high-yield savings accounts were paying an APY (annual percentage yield) above 5%. By comparison, the average interest rate for all savings accounts stood at an unimpressive 0.47% in January 2024, according to the Federal Deposit Insurance Corp. (FDIC)

| Brand name | APY* | Min. balance to earn APY | |

|---|---|---|---|

| Western Alliance | 5.31%† | $0.01 | VIEW OFFER |

| Bread Savings | 5.15% | $100 | VIEW OFFER |

| CIT | 5.00% | $5,000 | VIEW OFFER |

| SoFi | 4.60% | $5,000 | VIEW OFFER |

3. Money market accounts

A money market account – another type of savings account – is another way to potentially earn substantial interest.

In March 2024, the average interest rate for a money market account was 0.66%, according to the FDIC. That’s well above the average rate for traditional savings accounts. As of March 2024, some money market accounts were offering an APY above 5%.

There’s a trade-off for the higher interest you can earn on a money market account, though. These accounts generally restrict the number of transactions you can make by debit card, electronic transfer or check.

| Bank | APY* | Min. deposit | Monthly fee | |

|---|---|---|---|---|

| CIT | 1.55% | $0.01 | $100 | VIEW OFFER |

4. Certificates of deposit (CDs)

CDs are a type of savings account that locks up your cash for terms between three months and five years. For this reason, they’re a bit less popular than high-yield savings accounts. Nonetheless, a CD can pump up your savings thanks to high APYs.

As of March 2024, the average interest rate for a one-year CD was 1.83%, according to the FDIC. However, a number of one-year CDs as of this writing were promoting APYs above 5%.

| Brand name | APY* | Term | |

|---|---|---|---|

| Bread Savings | 5.50% | 12 months | VIEW OFFER |

| Barclays | 5.00% | 12 months | VIEW OFFER |

| Discover | 4.70% | 12 months | VIEW OFFER |

A big drawback to CDs is that you typically must lock in your money for a certain period of time. Otherwise, you could lose interest in the form of an early withdrawal penalty if you take out money before the end of the CD term. Generally speaking, you should put cash in a CD only if you’re certain you won’t need the money during the CD term.

Despite any disadvantages, the U.S. Securities and Exchange Commission (SEC) touts CDs as one of the safest options for savings.

5. Workplace retirement plans

Millions of American workers contribute to retirement plans set up by their employers.

So, what is a workplace retirement plan?

A workplace retirement plan lets employees contribute some of their pay to an account that invests in things like stocks, bonds, mutual funds and exchange-traded funds (ETFs). In some cases, the employer might match your contributions.

One of the most common workplace retirement plans is the 401(k), which is available to private-sector employees. Among the benefits of a 401(k) is its tax advantages. For example, contributions to a traditional 401(k) are made on a pretax basis, thus reducing your current taxable income. Taxes are due on any withdrawals from a traditional 401(k).

Among other workplace retirement plans are:

- 403(b) plans, designed for employees of public schools and certain charities.

- 457(b) plans, geared toward employees of state government agencies, local government agencies and certain tax-exempt organizations.

- Simplified employee pension (SEP) plans, enabling business owners to contribute to their employees’ retirement savings and their own retirement savings.

- SIMPLE (savings incentive match plan for employees) IRAs, letting workers and employers contribute to traditional IRAs set up for employees.

- Solo 401(k) plans, allowing self-employed people to put aside money for retirement.

For the 2023 tax year (that ends in April of 2024), you can contribute up to $22,500 to 401(k), 403(b) and some 457(b) plans. In addition, someone who’s at least 50 years old can make a catch-up contribution of $7,500. Different contribution limits apply to SEP, SIMPLE and solo 401(k) plans.

If you’re unsure what type of workplace retirement plan is available, check with your employer’s HR department or your manager.

6. Traditional IRAs

A traditional IRA (individual retirement account) lets you put money in a retirement account on a tax-deferred basis, and your money grows on a tax-free basis. This means you don’t pay taxes until you withdraw money from the IRA.

You can open a traditional IRA on your own (without your employer being involved) at places like banks and investment firms. This IRA can be paired with a workplace retirement plan to boost your savings.

Among the kinds of investments available with a traditional IRA are stocks, bonds, mutual funds and ETFs.

For the 2023 tax year, the IRS limits IRA contributions to $6,500. For the 2024 tax year (you file in April of 2025), the IRA contribution limit is $7,000. Someone 50 and over can tack on a catch-up contribution of $1,000.

7. Roth IRAs

A Roth IRA allows you to put money that’s already been taxed in a retirement account. Your money grows on a tax-free basis, and eligible withdrawals during retirement are tax-free.

Just like a traditional IRA, you can set up a Roth IRA on your own at banks, investment firms and other financial institutions. You can own a Roth IRA and a traditional IRA at the same time. These accounts can be coupled with a workplace retirement plan to supersize your retirement savings.

The types of investments you can make through a Roth IRA include stocks, bonds, mutual funds and ETFs.

Roth IRAs have the same contribution limits for 2023 and 2024 as traditional IRAs. It’s worth noting that if you have both a traditional and Roth IRA the total contribution to both of them, however you decide to split it up, is still $6,500 for 2023 and $7,000 for 2024. The limit also includes your catch-up contributions.

8. Stocks

When you buy a share of stock, you’re buying an ownership stake in a company whose stock is traded on an exchange like the Nasdaq or the New York Stock Exchange. If you purchase a share of stock in McDonald’s, for example, you’re essentially a co-owner (however small) of the restaurant chain.

Stock prices go up and down based on several factors, such as a company’s performance and overall economic conditions. As a result, you can benefit from an uptick in a company’s stock and be hurt by a downturn. Some companies share their profits with stockholders in the form of dividends.

You typically can buy stock through a brokerage firm like JP Morgan, Robinhood, or Fidelity Investments. The stock can be kept in an investment account at the brokerage firm or even be included in an IRA.

Some brokerage firms charge commissions on stock trades, but many firms offer commission-free trades. Keep this in mind when you’re looking for a place to trade stocks.

Stocks are considered a risky investment, as they can lose some or all of their value depending on the fortunes of the company and the stock market. On top of that, buying and selling individual stocks requires regular homework on your part so that you can increase your gains and minimize your losses as much as possible. Nevertheless, if you have faith in the future prospects of a company, smart stock trading can lead to healthy rewards.

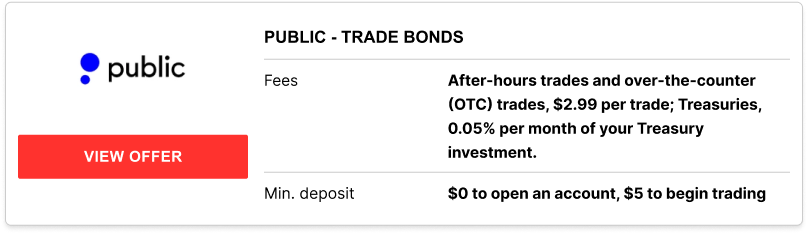

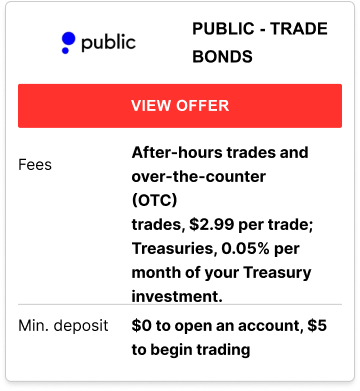

9. Bonds

A bond is a type of debt that’s similar to an IOU, which is how the SEC describes it.

“Borrowers issue bonds to raise money from investors willing to lend them money for a certain amount of time,” the SEC says.

When you buy a bond, you’re lending money to the issuer, which may be a government, municipality or corporation. In exchange, the issuer promises to pay you a certain rate of interest during the life of the bond and to repay the principal when the borrowing period ends.

Bonds carry risks, such as losing all the money you invested if the borrower defaults on its bonds. However, bonds are considered safer investments than stocks. This safety comes at a price, though. The investment returns on bonds tend to be lower than those for stocks.

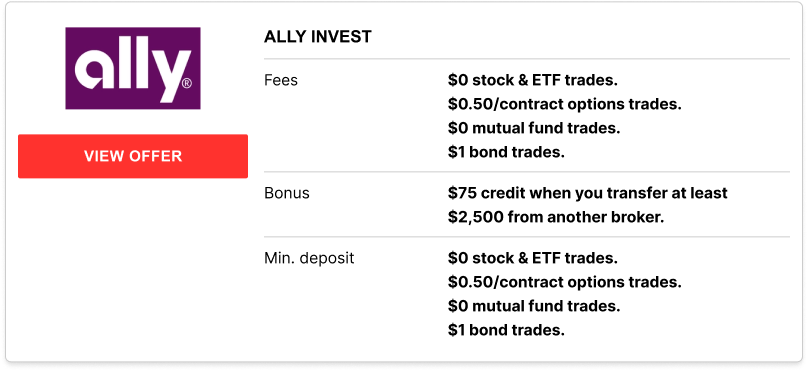

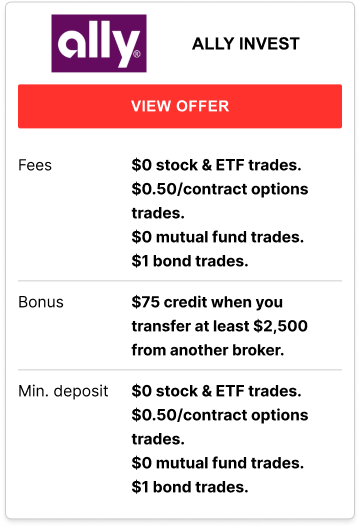

10. Mutual funds

A mutual fund is a pool of investments in things like stocks and bonds. When you purchase a share of a mutual fund, you’re spreading your risk across a variety of investments. Professional money managers decide when to buy and sell assets included in a mutual fund.

Mutual funds are attractive investments because they provide access to a variety of asset types. Furthermore, mutual funds take the guesswork out of picking individual stocks and other individual investments.

However, mutual funds come with risks, such as a potential drop in the value of the mutual fund shares. These shares are not traded on stock exchanges; you have to buy shares from the fund itself. Sometimes you invest in a mutual fund because it’s offered by your retirement plan or because you have an account with a mutual fund provider like Vanguard. Fund shares are repriced once a day and depend on the value of the assets owned by the fund.

Among the providers of mutual funds are brokerage firms like Ally Invest, Charles Schwab, Merrill Lynch (Bank of America) and Vanguard Group.

11. Exchange-traded funds (ETFs)

Similar to mutual funds, ETFs offer access to pooled investments like stocks and bonds. But unlike mutual funds, shares of ETFs can be bought and sold throughout the trading day on a stock exchange.

As with mutual funds, ETFs provide access to a “basket” of assets, allowing you to diversify your portfolio. Each fund generally sticks to a certain kind of investments, such as stocks of foreign companies and stocks in a certain sector (like energy), though there are ETFs that invest in the total stock market and actively managed ETFs that only own a handful of assets.

Among the providers of ETFs are iShares, Invesco, Charles Schwab and Vanguard Group. ETFs normally are a low-cost type of investment. However, some funds might charge sales commissions or management fees.

If you’re a beginning investor, an ETF can be a solid option because you don’t need to buy or sell individual stocks or other individual investments. Still, if you hold ETF shares, it’s smart to keep an eye on the trading activity so you can protect your capital investment.

2 Cards Charging 0% Interest Until 2026

With no annual fee and no interest until 2026, this card is helping Americans pay off debt in record time.

Advertisement: CompareCredit

Advanced Options Trading

Access Cboe® index options on a trading platform built for traders.

Advertisement: CompareCredit

Cboe® Index Options

Advertisement: Trade Station

2 Cards Charging 0% Interest Until Nearly 2026

Advertisement: CompareCredit

Top Doctors 'Anti-Lazy' Drops Are Going Viral This July

Advertisement: Health Headlines